SNAP is a short-term “trading buy”/long-term “avoid”.

SNAP is a short-term “trading buy”/long-term “avoid”.

Trading Opportunity:

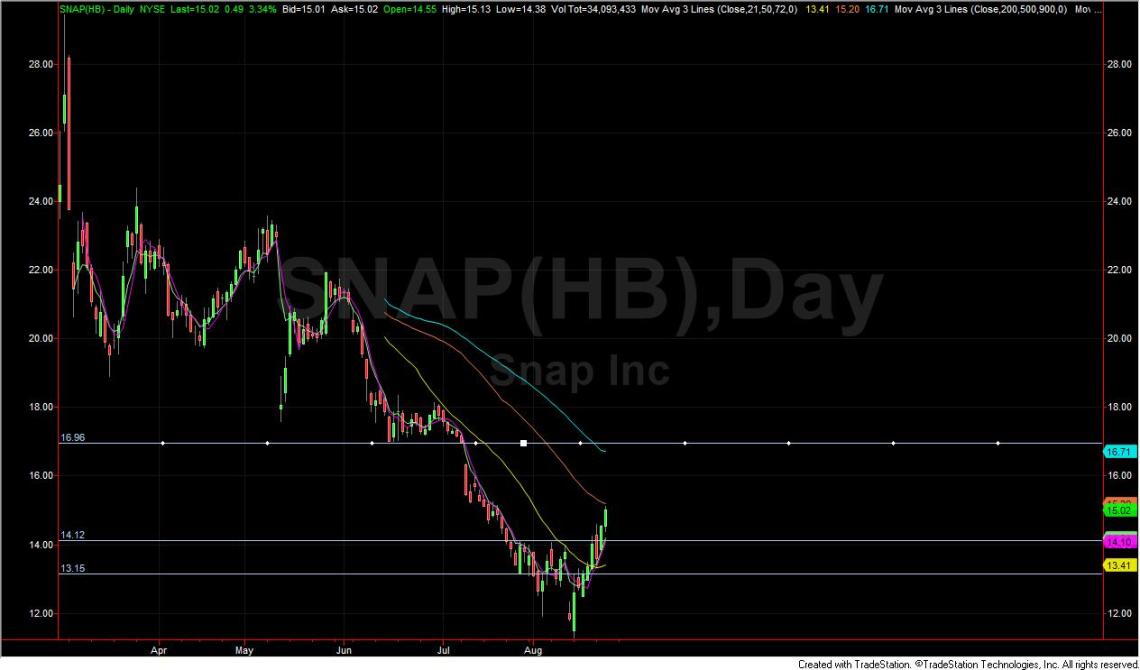

As I discussed in my previous post, SNAP was due for a “snapback” rally. A stock with that much hype and institutional support will have buying opportunities on its way to a more appropriate (lower) valuation. SNAP reached a price (11.28) that traders and investors found attractive after the Q2 earnings release and on the exact date of the second share lockup (August 14th). It gave a low risk entry at 12.38 on August 14th on a prefect retest after an hourly demand bar on the hourly chart where you could have entered with a stop below the lows at 11.28. Risking 1.10 to make 2.62 at the current price of 15. SNAP may continue to the gap fill and resistance at 17, but if I were long, I would be looking to sell a that level until it proves it can trade convincingly above that strong resistance.

Valuation:

On a valuation basis, SNAP is a different, more complicated story:

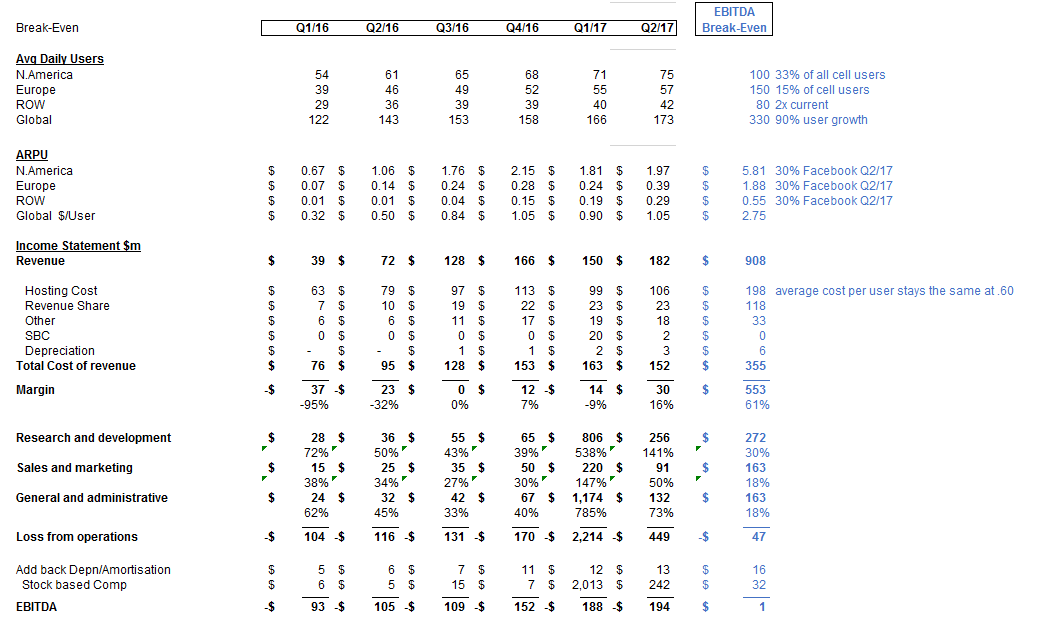

In Q2 2017, not only did SNAP miss on users and revenue, it has a bigger problem. There is no credible path to profitability. In the most recent quarter, (Q2/17) SNAP lost $485m on revenues on $182m. Building a model where SNAP is EBITDA break even requires every variable to be pushed to the edge. Even if we suspend reality for a moment and assume that this can be done, how long it would take to get there? Realistically, competitors such as Facebook (Instagram) are not going to sit back and let that happen without a fight as we have already seen with Instagram coping SNAP’s features including “stories”.

What would it take to just Break-even at the EBITDA Level?

Although SNAP’s stock price is currently 23% below the IPO price, it still has a market cap of $16bn (Aug 22th) . This, for a company hoping to generate $800m in revenue (FY2017) and that is projected to lose more than $3b this year. Thus, it appears investors would like to believe that there is the potential to generate significant income in the future. Taking an optimistic view with significant growth in daily users, and very aggressive growth in revenue per user, we see the EBITDA break even around $900m/qtr of revenue. This is 5x the revenue in the most recent quarter, possibly achievable in 2 years with the current high growth rates.

With SNAPs 1.2bn shares currently outstanding (and growing with their fondness for stock based compensation), making just 1c/share in a quarter requires $12m of net income (not EBITDA). Justifying that stock price is not going to be easy.

- User growth and potential

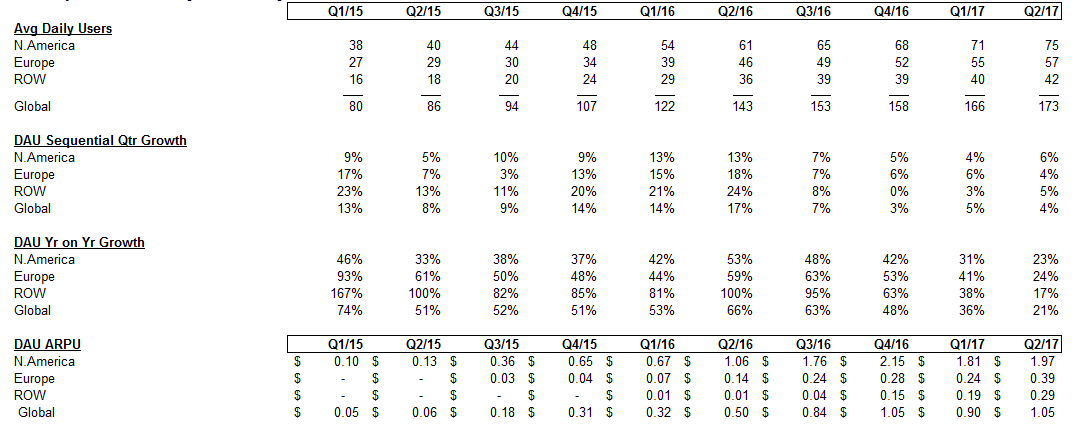

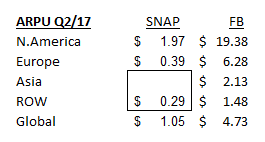

SNAP currently has 173m daily average users. SNAP’s users are exclusively mobile as it is only available on mobile devices. In Q2/17, SNAP has 75m users in North America. Given that there are approximately 300m cellphone users in North America, of which 80-85% have smartphones, SNAP already has 30% of the total addressable market using the app daily. Bearing in mind that 60% of SNAP users are aged 13-24 (or younger) and 86% are 13-34 (www.statista.com/statistics/326452/snapchat-age-group-usa/), having 30% of North.American cell subscribers using SNAP daily is impressive. The problem is that even with those subscriber numbers, SNAP is far from profitable, in fact it is burning money. Adding daily users outside the 13-34 age group is going to be much tougher. Part of the attraction of SNAP for the 13-24 age group is that their parents are not using it. In fact, 30% of SNAP users admit to using the service because their parents do not use it, growing the user base beyond the 13-34 demographic may encourage the core users to move on to something else.

Outside North America, SNAP has 57m daily users in Europe and 42m in the rest of the world. With 2.1bn smartphone users outside North.America, there is plenty of potential upside here. However, SNAP is not a service that scales well. On average each SNAP active user costs $0.61 per quarter to cover the bandwidth, storage and server hosting. The users outside North America only generate $0.35 per quarter of revenue, so attracting more users in many markets may be a burden rather than a path to profitability. Losing money on every sale, but making it up on volume is a tricky strategy to pull off.

- Revenue per user:

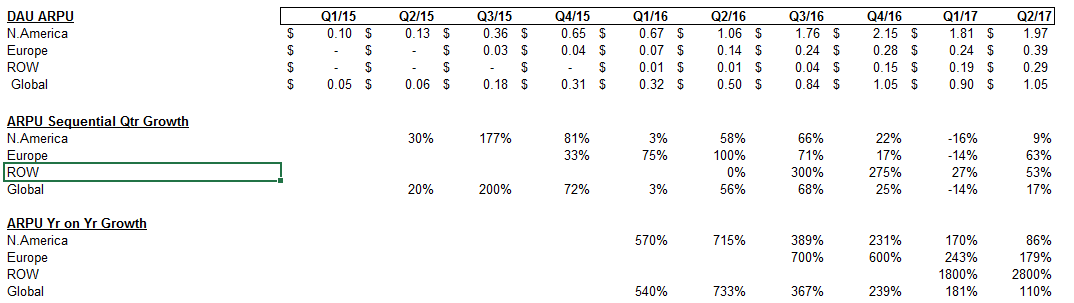

The average revenue per user has been in the $0.84 – $1.05 range for the last four quarters. The ARPU per customer is likely to grow based on the screen time per user, advertising sales tools and product development. How much upside is the question.

Facebook currently generates $4.73 per user quarterly. In North America, Facebook generates almost 10x the SNAP revenue per user. Reaching these levels is unlikely for SNAP with the platform and target users (13-34 year olds) they have. Facebook users are older, and more valuable to advertisers than SNAP. Facebook is also used across multiple devices.

- Hosting cost per users: SNAP has outsourced hosting to Google, and has recently added AWS. There is a commitment to Google to spend $2bn over 5 years, and smaller commitments to AWS. Outsourcing is not a bad idea in itself. Building and managing data centres, commissioning servers and developing a networks capable of handling the rapid user growth would consume considerable capital and resources. The Google cloud model will keep costs more or less variable, although it will reduce EBITDA vs investing in SNAP’s own facilities.

SNAP is a high bandwidth and resource intensive application. Users upload 3bn snaps and consume 10bn short videos per day. Much of the content self destructs after a short period (part of the attraction to the younger users) reducing storage costs, but it still consumes a huge amount of bandwidth and processing power. Much of the traffic will be originating or terminating through the cell networks, with whom Google will peer directly controlling bandwidth costs. Based on 50mb per day per user (from our own tests with fairly light usage), the bandwidth alone would cost $0.10-0.20 per user.

Bandwidth costs will continue to decline over time and there will be some volume benefits, but the high user engagement that advertisers will want to see is going to keep these costs per user in the $0.60 range.

- Revenue share: Some advertising revenue is through sales partners who receive a revenue share. This expense is reported as a cost of sale has been running at 13-15% of revenue. SNAP will be looking to reduce this over time and do a higher proportion of direct sales.

- SG&A, R&D and G&A:

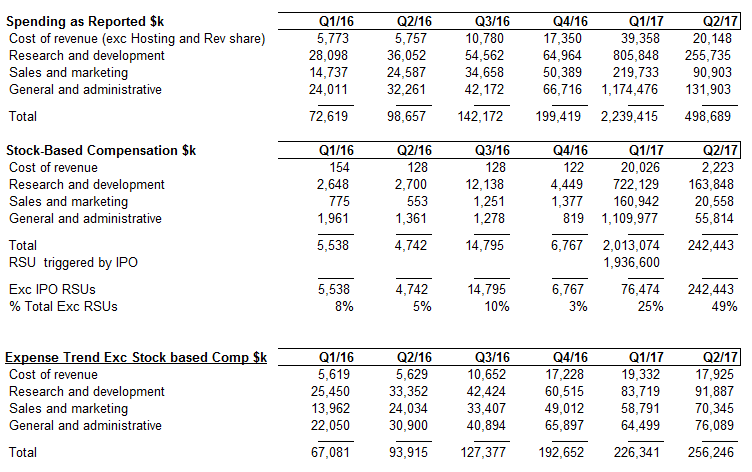

The current levels of expenses reflect the efforts to grow rapidly. They include considerable stock based compensation, and in Q1 and Q2 of 2017, the impact of the vesting of the RSUs triggered by the IPO added $1.9bn and respectively to expenses. Even excluding stock based compensation (which is likely to be an ongoing real expense for years to come), the level of spending currently bears no relation to the current revenue and any analysis is meaningless. Over time as the top line grows, they will presumably drop to something more comparable with their peers, but even assuming this, the profitability is not evident.

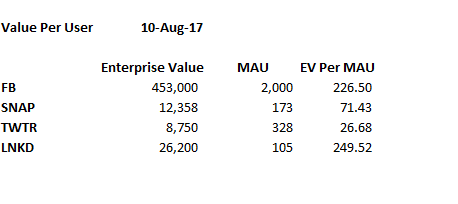

Value per User

Some may argue that Snapchat is valuable on an enterprise value per user basis. Comparing SNAP to FB, LNKD (takeout value), and TWTR, that doesn’t seem to be the case. LinkedIn got taken out at $249 per MAU, but was generating $7.14 in quarterly revenue per MAU, and was EBIT positive. FB is valued at $226 Per MAU with $4.50 in quarterly revenue per MAU. TWTR, while is generates $1.75 per MAU has an EV per MAU of $26.68. SNAP is no bargain at $83 per MAU while generating $1.05 in quarterly revenue.

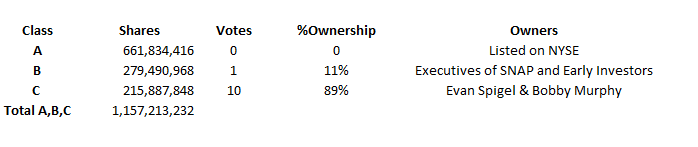

Share Structure and Governance

Even if the financials showed potential, this stock would have some major yellow flags given the capital structure. SNAP has issued A, B, C shares. The publicly listed share have no voting rights. The two founders, Evan Spiegel and Robert Murphy control 88% of the company.

Conclusion:

All in all, on any metric, it is difficult to justify recommending the purchase of Snapchat on anything other than a trading basis.

Risk to Thesis:

The risk is that someone takes out SNAP at a nonsensical valuation. Liquidity is still high, companies are flush with cash and social media is a popular trend. It has happened before (remember AOL and Broadcast.com).